Focus: China Bonds Attractive to Asset Allocators

Guillaume Page

April 1, 2019 marked an important date for China, not because of a new “tweet” by President Trump about tariffs or because of a new investigation by foreign authorities into Chinese companies, nor because it was April Fool’s Day. April 1 was the effective date that onshore Chinese government bonds were included into the Bloomberg Barclays Global Aggregate Index. This inclusion is just one component of the long term gradual integration of China’s debt market into the global capital market system and a catalyst for China’s goal of increasing the global importance of its currency.

China’s bond market size is approximately USD 12.5 trillion and it is on track to exceed Japan as the second largest, but China’s bond market is likely to still remain in second place behind the United States. The inclusion of Chinese bonds in global bond indices will occur gradually and progressively through and until November 2020. By then, China could represent more than 5% of global bond indices, and in effect elevate the role of the Chinese yuan (RMB) as a major competing currency versus the US dollar, euro and Japanese yen.

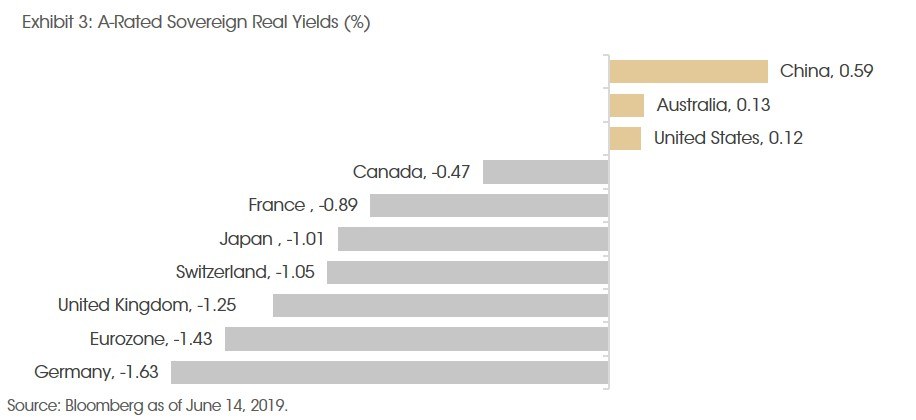

For China, this is a step forward for further opening of its capital market. More importantly this represents an opportunity for investors globally to improve their access to a market that has potential for growth. One measure showing the attractiveness of this asset class is the current real yield across major markets. [See Exhibit 3.] Onshore Chinese sovereign bonds are unique in that they are currently rewarding investors with positive real yield. Real yield takes into account inflation. In 2018, it was one of the few asset class to generate positive return (approximately 8% yield in RMB terms). During the last decade, Chinese domestic bonds have generally achieved investment returns comparable to other emerging markets, and volatility has been somewhat similar to developed markets. After all, the onshore Chinese bond market is currently dominated by domestic investors. Consequently, it has near zero or negative correlation to other major bond and equity markets.

In recent years, global central banks continued monetary easing policies, which drove ever lower returns for even safe credits. Based on the current environment and our views, we don’t think yields globally will likely increase significantly in the near-term and furthermore we think that China’s real yield should continue to stay above peers. China’s instruments are likely to be one of the few positive earners. We believe that this is one of key drivers that is lending attention of foreign investors’ asset allocation into RMB bonds.

However, challenges exist as China continues the advancement of its capital market. China still needs to enhance its accessibility, specifically the arrangement and solid infrastructure of the various access schemes, such as the China Interbank Bond Market and the Bond Connect. In addition, transparency is another challenge for foreign investors because Chinese issuers and parents are still evaluated by domestic agencies and not by established foreign credit rating agencies. The access of foreign credit rating agencies has long been a contingent point in the early days of what became trade tensions between President Xi and President Trump. Consequently, Chinese authorities have just approved Standard & Poor’s Global, a leading international rating agency, as the first foreign credit rating agency that is permitted to score Chinese onshore bonds.

It is likely that over time foreign investors will have a higher participation in the Chinese bond market, and this will act as an accountability mechanism which is likely to drive progressively reforms to the regulatory framework of China’s capital market. As investors, we think that the risks for investing into this asset class exceed the benefits, even though onshore domestic bonds could bring value to a diversified allocation, as Exhibit 3 shows. The growing importance of China’s capital market should not be overlooked by global asset allocators.

As a Chinese proverb says, “Be not afraid of growing slowly; be afraid only of standing still (不怕慢,只怕站)”. Only the coming years will tell if China will continue this transition or pause.

Sources: Bloomberg and CIGP Estimates.