CIO Viewpoint: 2021 Outlook - Reopen to Recover

The global economy is estimated to have contracted by around -4% in 2020 due to the pandemic-led lockdown and mobility restrictions. However, two factors differentiate this crisis from the previous ones.

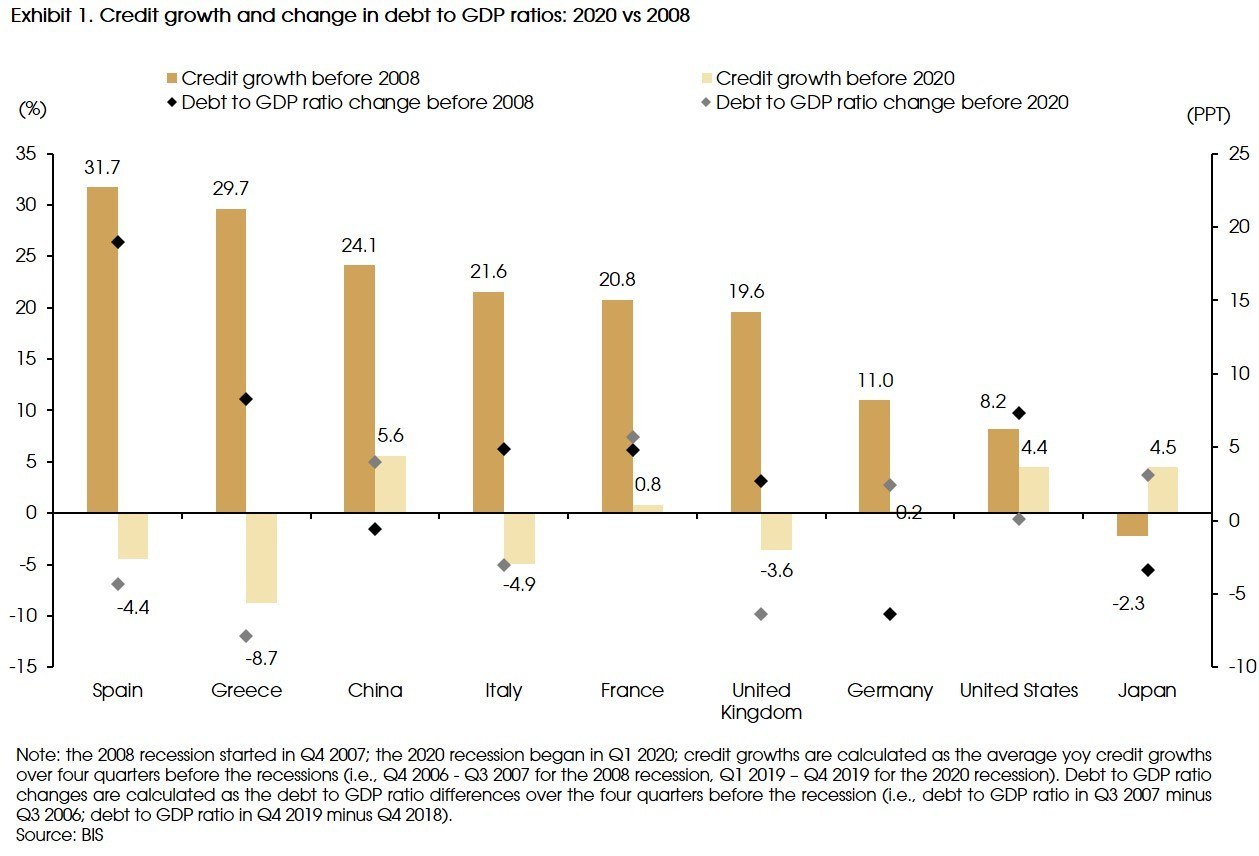

First, this crisis is mainly caused by exogenous shocks, not by endogenous economic factors such as rising inflations or interests, nor by collapsing asset prices or debt accumulation. Specifically, unlike the credit-boom-induced crisis in 2008, credit growths to private sectors stayed low or even negative in major economies before the current recession, while prior to the 2008 crisis, credit growths were much higher at around 10% in the US and Germany and well above 10% in many other European countries (Exhibit 1). Moreover, debt to GDP ratios were generally declining in most economies before the pandemic but rising prior to the 2008 financial crisis.

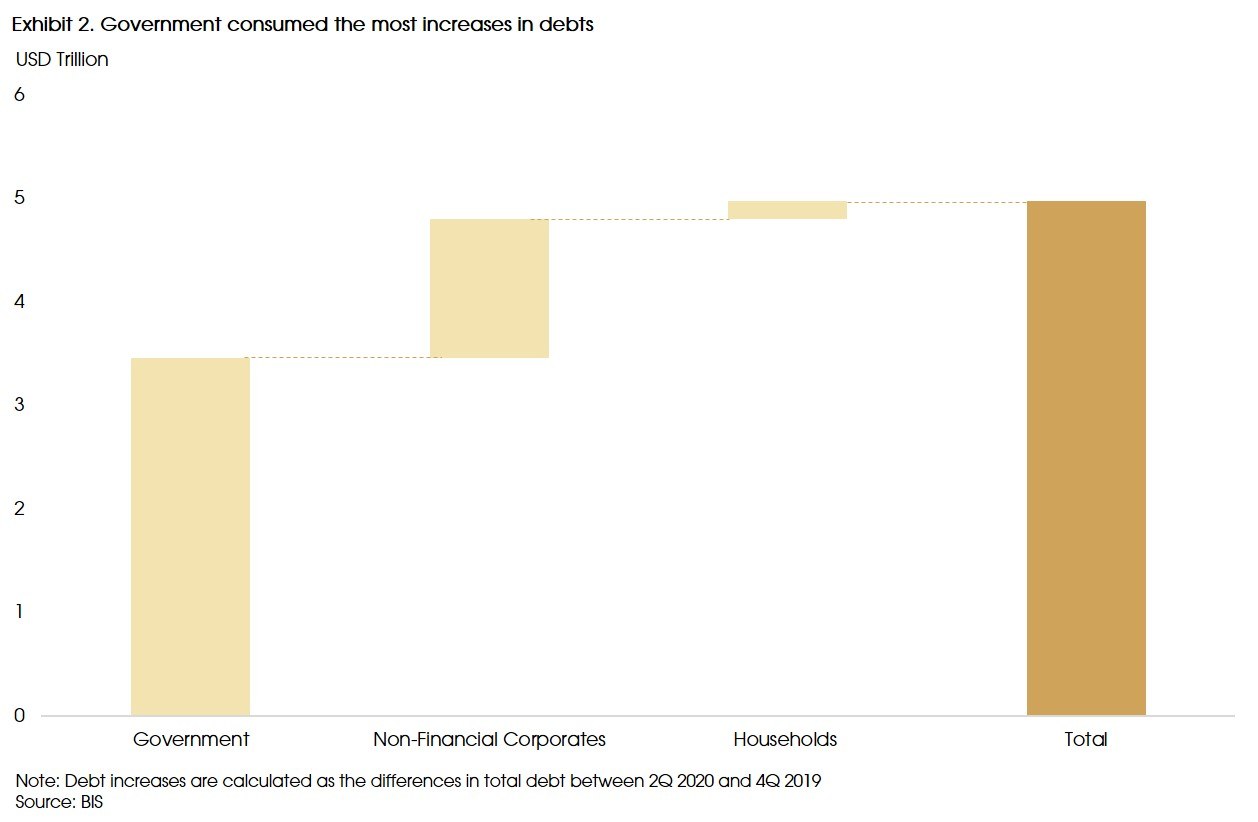

Second, given the nature of the current recession, policymakers are less worried about controlling the leverages in private sectors or about the sovereign debt stress of governments, expecting a quick recovery can more than offset the rising debt levels caused by the recession. As a result, both monetary and fiscal policy actions are unprecedented in both size and speed, and the debt increase after the pandemic was mainly concentrated on governments (Exhibit 2).

The increased government spending was used to support households' income and reduce the liquidity pressures for enterprises. Such policy supports have prevented a significant surge in private sector debt and managed to restore the confidence of companies and individuals, by reducing the scarring effects on the economy.

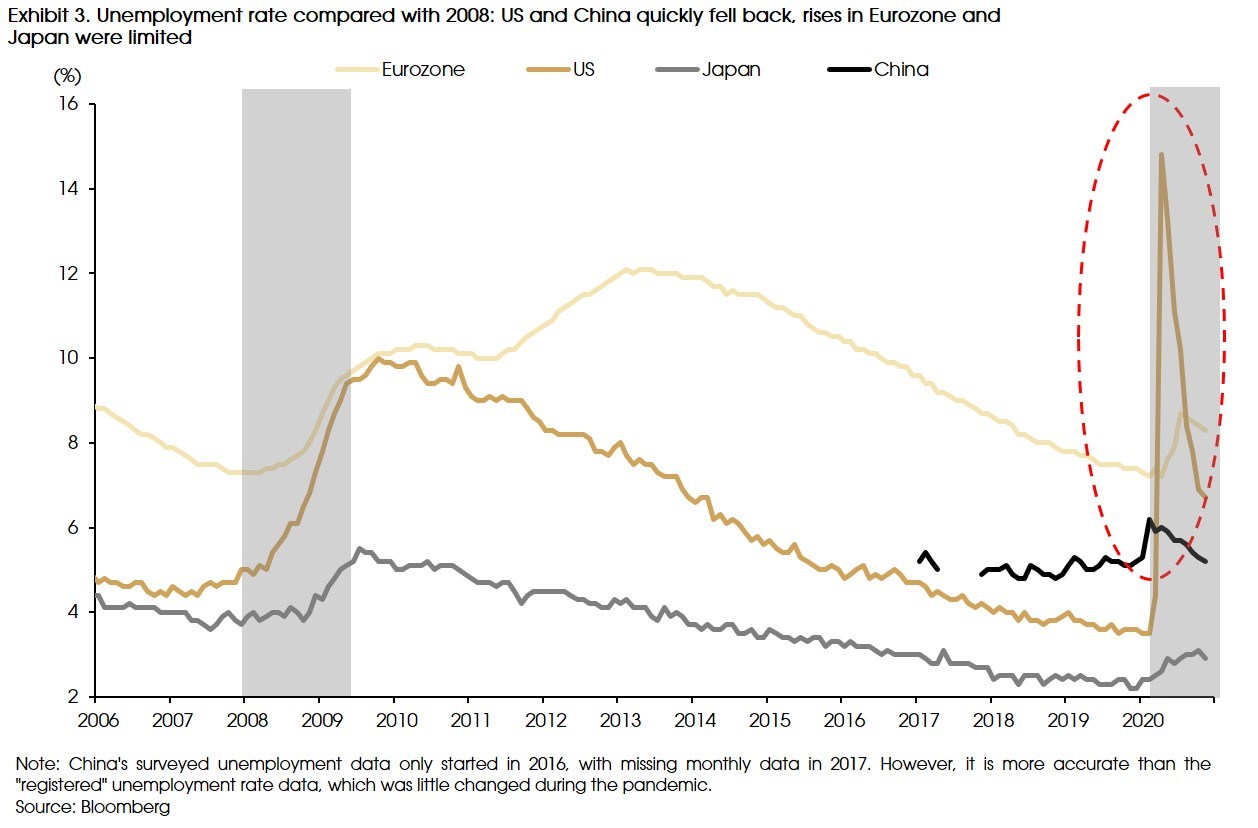

For example, In the labor market, most advanced economies, such as Eurozone and Japan, have successfully used generous wage subsidies and job retention programs to contain the rise in headline unemployment rates (Exhibit 3). In countries where unemployment has risen sharply, such as the US, the increase has primarily come in the form of temporary layoffs. As many of these temporary job losers can be brought back to work quickly, the headline unemployment rate went down by nearly 8% in 8 months, much faster than the "unemployment normalization process" seen in the previous recession.

The business sector has also coped with the current economic downturn better than expected, given the efforts by central banks and policy makers to keep credit flowing. In sharp contrast to the significant increase of bankruptcies after the 2008 financial crisis, the number of bankruptcies actually went down last year in many major economies (Exhibit 4).

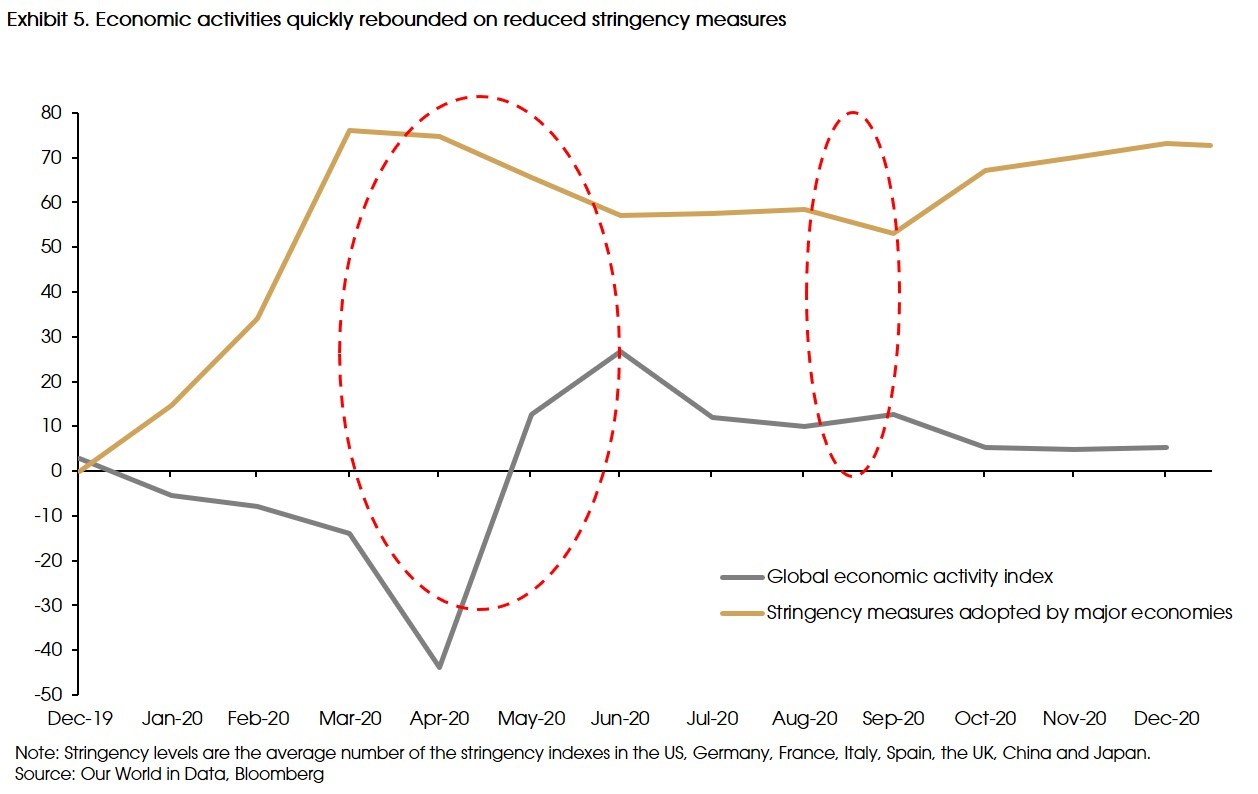

Such policy supports are not only for "hiding" the rising numbers of unemployed and bankruptcy. By keeping individuals from "permanently" losing their jobs and enterprises from going bankrupt, employees can be quickly brought back, and businesses can quickly resume once the containment measures are lifted. Global economic activities have shown quick recoveries in April-May and August last year, as the stringency levels of the containment measures decreased (Exhibit 5).

1. Reopen to recover: a quick but bumpy bottom out

Given the unique nature of the pandemic-led recession and the ultra-accommodative policy support, which have significantly reduced the long-term scarring effects in the economy (i.e., rising private sector debt, unemployment and bankruptcy), we may see a quick rebound in economic growth in 2021. However, the strength of the recovery will highly depend on whether the vaccination process can bring the virus under control and how quickly the economies can achieve a complete reopening.

Major economies are expected to bottom out from the deep troughs in 2020, and the global GDP growth may increase from -4% last year to 4-5% in 2021 (according to the IMF and the World Bank). In our view, growth differences between major economies mainly result from four factors:

- Pandemic control: this is still the most important driver for the recovery this year, better control means faster and more complete economic reopening, which leads to higher growth.

- Pre-pandemic growth momentum: as the recovery is a "return to normal" process, pre-pandemic economic conditions can be a good reference for the recovery. A solid pre-pandemic economic condition may lead to a stronger recovery.

- Policy support: more policy support (especially fiscal stimulus) will lead to stronger recovery.

- Exposure to the pandemic-sensitive sectors: as cross-border travel may be the most affected sector by the pandemic, and would be the last to recover. Therefore, higher exposures to tourism sector will lead to slower recovery.

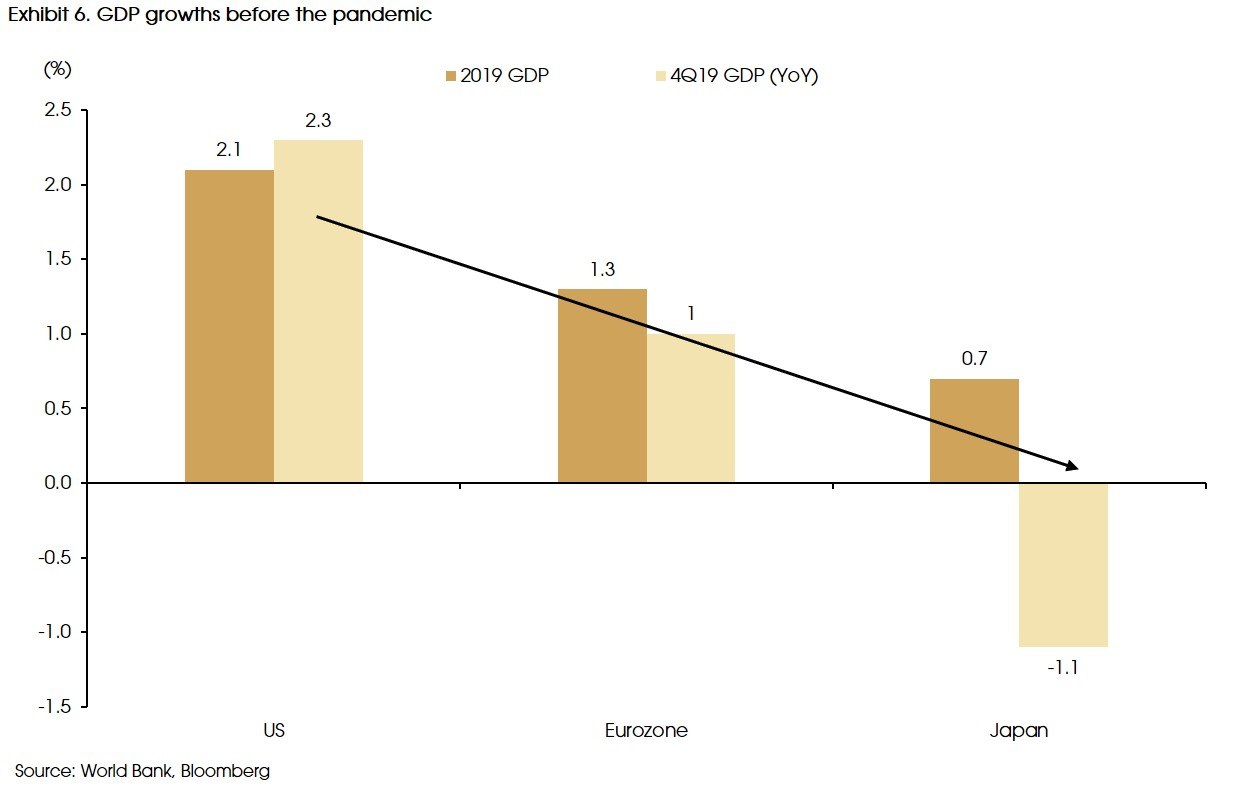

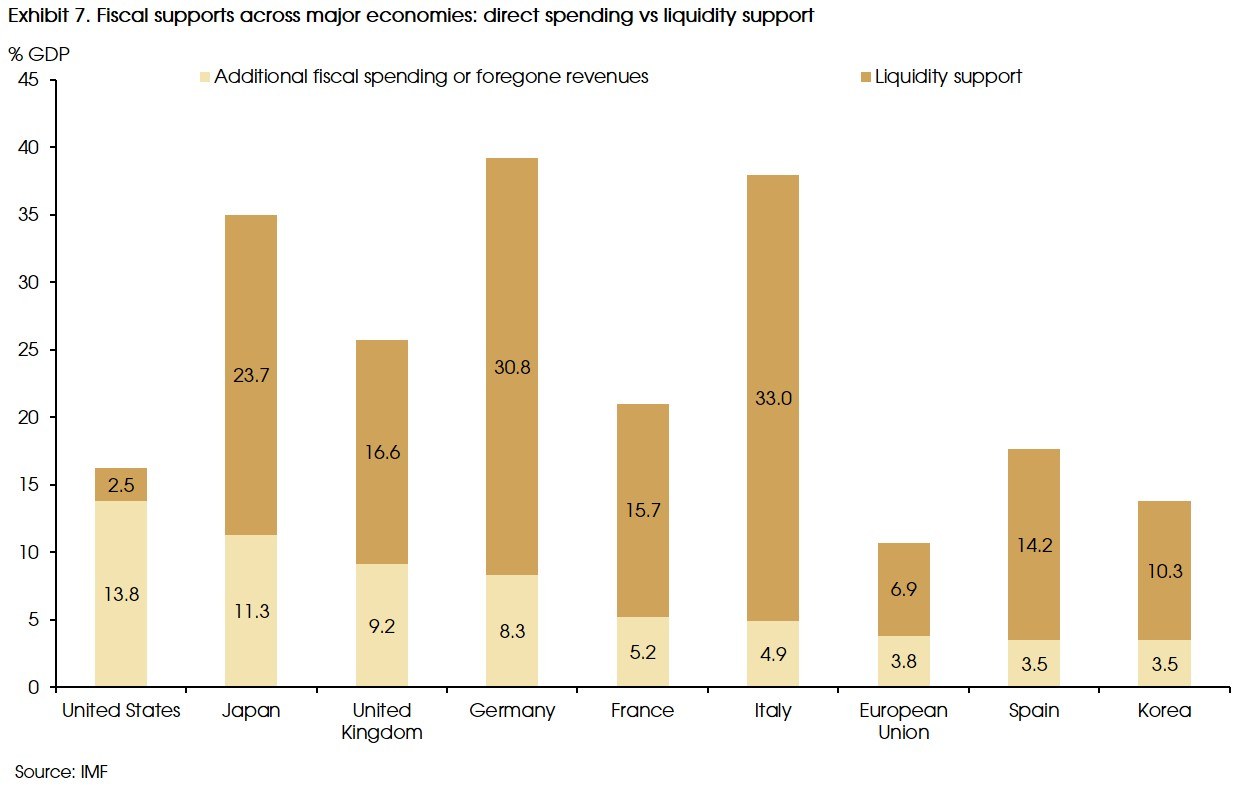

Based on these factors, China will have a much stronger recovery, given its successful pandemic control. The US will also have a more solid recovery than the other developed economies due to its stronger economic condition before the pandemic (Exhibit 6.) and more direct fiscal support compared with other economies (Exhibit 7). However, considering that Japan's economy already fell into recession before the pandemic (GDP growth at -0.7% YoY in 4Q 2019), while the Eurozone's growth was also stalling and more sensitive to the tourism sectors, the recoveries for these two regions will be weaker.

Risks to this quick rebound of economic activities are generally balanced to the downside, mainly resulting from the uncertainties regarding the pandemic path and the effectiveness of the vaccines.

Rising debt ratios in corporate sectors also merit further attention. However, we think that most of these companies are illiquid ones rather than the zombie companies seen in the previous credit-boom-led recession. Moreover, given the credit support from central banks and governments, we do not expect to see debt crises in major economies. However, a prolonged lockdown might turn these companies into unviable ones. Therefore, we think that solvency risks should remain secondary, at least for now.

On policy side, both fiscal and monetary policies should remain accommodative to support the recovery. Specifically, given the deep recession in 2020, and the considerable uncertainties regarding the pandemic path, the vaccination, and the recovery, we do not expect to see tightening policies to be rolled out this year, such as the tax hike from the Biden government, nor the rate hikes from major central banks.

Moreover, on trade policies, we do not expect to see serious trade conflicts among major economies, but more regional collaborations. Specifically, the US-China relation may improve under Biden's presidency, given his multilateralism. However, complete normalization in US-China trade relations is also unlikely, as the US's hawkish stance towards China is one of the bi-partisan agreements in recent years.

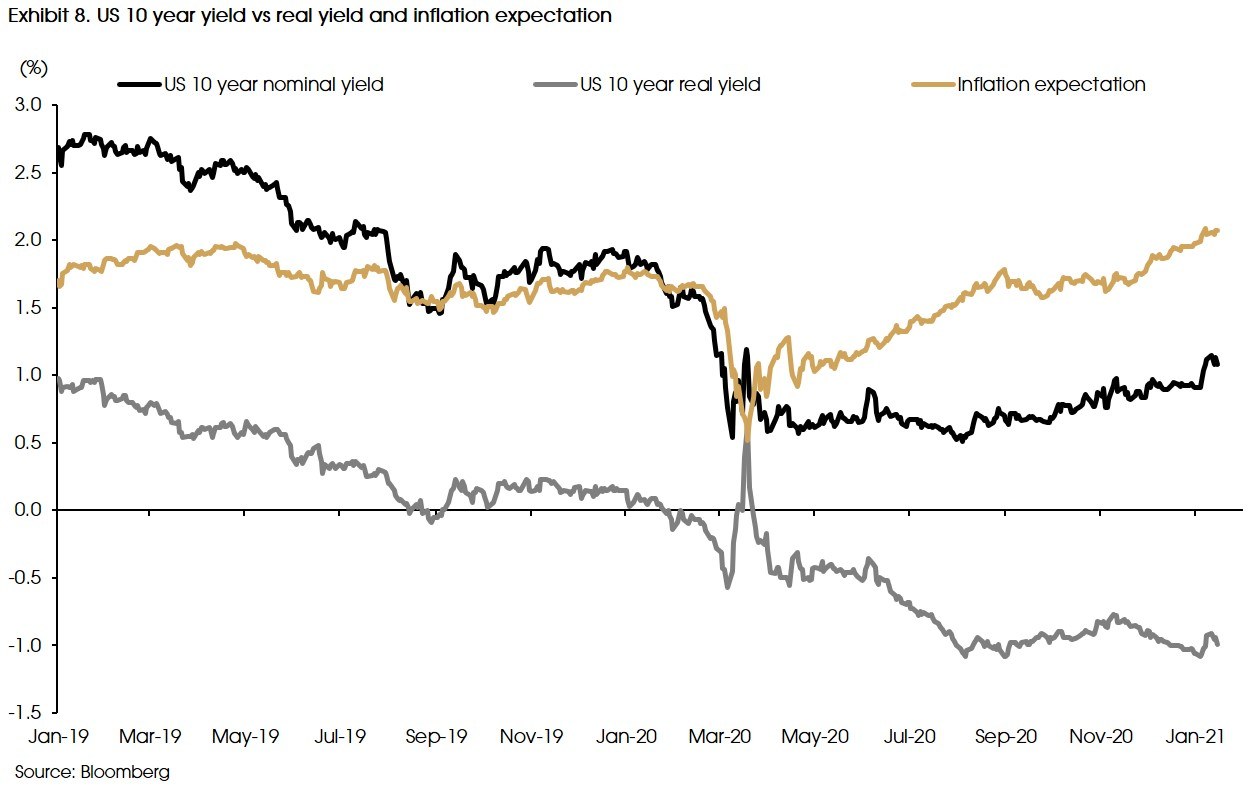

With the large scales of stimulus policies supporting the demand, while the supply-side production facing more risks alongside the recovery, inflation will rise and drive up interest rates, especially in the US. However, the Fed's continued bond purchase should cap the long-term interest rate. Therefore, the 10 year US treasury yield will remain under 1.5%. Meanwhile, due to the rising inflation expectations, the real interest rate will remain low and negative (Exhibit 8). Inflation pressures and rises in interest rates will be milder in the Eurozone due to its weaker growth momentum.

2. Growth and policy outlook favors risk asset, but volatility will increase

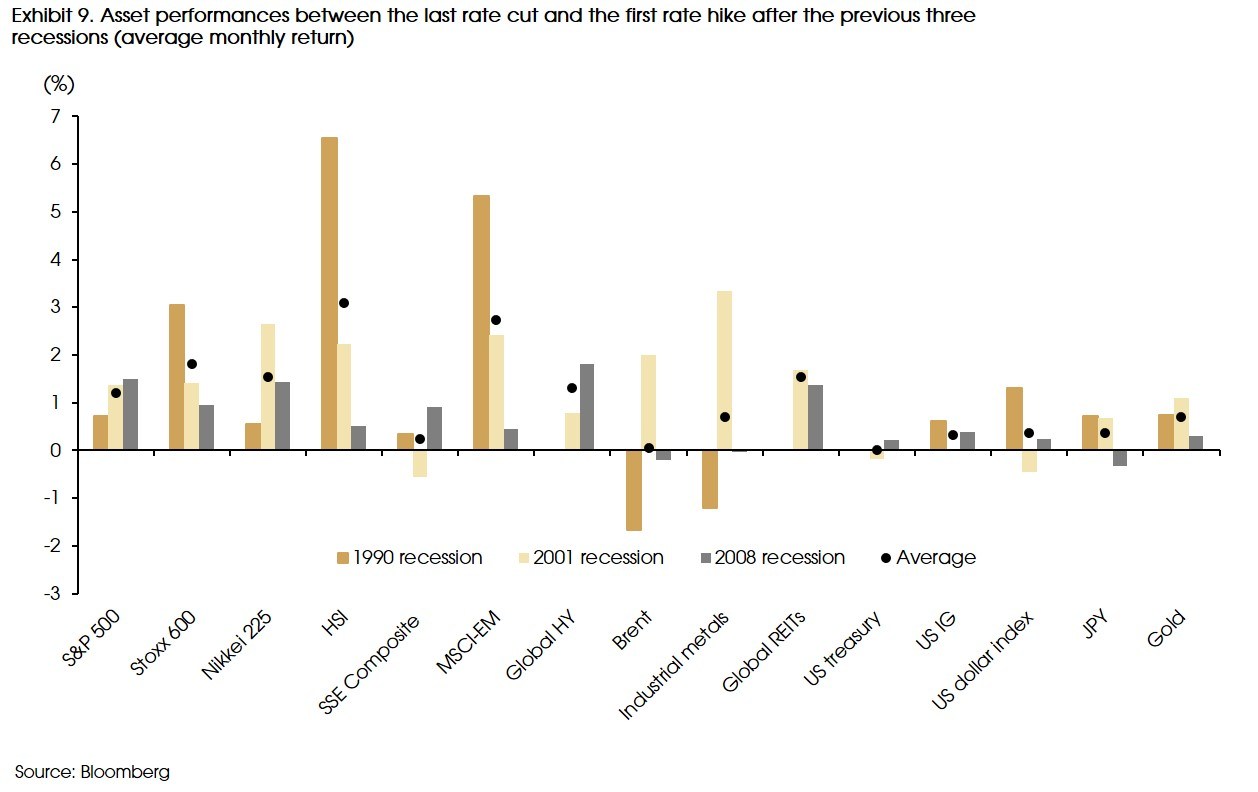

Given the expected economic recovery and the accommodative monetary and fiscal policies, equities may continue to outperform. For example, for the previous three recessions in the US, in 1990, 2001, and 2008, during the early recovery stages after the recessions (proxied by the period from the end of the Fed’s rate cut cycle to the start of the next rate hike cycle), equities always outperform (Exhibit 9).

However, instead of mainly driven by valuation expansion in 2020, equity performance should rely more on earnings growth this year, while valuation will drop. Given this “growth driven” phase, we are more positive on the US and Chinese markets due to their more solid growth outlook.

The transition between the two phases may lead to increased volatility in equity markets. However, in our view, significant and prolonged market downturns will mainly result from two extreme cases: 1) another recession in 2021, 2) a much faster than expected recovery which significantly drives up inflation and leads to monetary tightening from central banks. That said, these two cases are the two extreme scenarios in our prediction spectrum, and we do not see them as very likely to happen.

Cyclical sectors may catch up with the recovery and rising interest rates, but their performance also heavily rely on the strength of the regional economy and could be more sensitive to the pandemic path. Therefore, we see opportunities on the cyclical sectors in China but not much for the other markets. Moreover, different from some market views about the sector rotation from growth to cyclical / value, we still prefer growth stocks, even if they will be affected by the rising interest rates.

Bond markets may underperform given the rising interest rates, especially for the US due to its higher inflation pressures. That said, any worse than expected growths or pandemic paths in major economies could still lead to further rate cuts from central banks and drive up the bond prices, for example, the ECB recently signaled that further rate cuts are still on the table.

The supply shock from last year and the rebound in demand this year may lead to continued modest rising prices for commodities. Gold prices should also maintain its upward trend due to the negative real interest rates.

Finally, we expect the dollar weakness to continue given the narrowing US-Eurozone real yield gap (mainly due to the widening gap between inflation expectations). However, a number of factors could lead to a dollar rally. For example, a better outlook on the US economy and the associated reflation trade after Trump’s election led to a 6% increase in the dollar index, and Biden’s aggressive fiscal stimulus may result in a similar trend. That said, as long as the big picture of the global recovery does not change, such rallies should mainly focus on the short-run, as what we saw in 2017.

For the sectors that we like in the long term (i.e., tech, healthcare, consumer, and renewable energy), we see more opportunities in renewable energy and tech in 2021.

3. Renewables sector: notable capacity increase in solar

We are bullish on renewable energy for 2021, given the accommodative government policies and the ever-increasing demand from global corporations. In particular, we prefer solar (solar photovoltaic, PV). We think that solar will experience its largest global electricity generating capacity addition ever.

International agencies and research organizations estimate new solar installations this year will amount to between 150 and 200 gigawatts (GWs) of electricity generating capacity, exceeding the entire UK’s renewable and non-renewable electricity capacity in 2019This surge comes on the back of increased investments into solar, which rose by 12% in 2020 despite the economic slowdown. These investments have led to improvements in technology, which has reduced the costs of solar PV modules by 97 percent over the last four decades.

Favourable government policies globally will drive growth in 2021. In particular, most recent expectations are that China, Europe and the US will be ramping up their solar capacity with expected additions of over 40GWs in China and over 20GWs each in both Europe and the US. Direct consumer purchase of rooftop solar is also expected to become more of a trend, as countries like Germany and Australia provide tax credits for home installations.

Regardless of government policies, companies themselves are prioritizing the shift to renewables. The large US tech companies have led this initiative. Google, for example, wants to eliminate the need for fossil fuels altogether through matching the time of renewable energy generation to the time the energy is consumed. Corporations are also gradually looking to reduce scope 3 emissions. These are emissions caused by the production and use of their products. Apple, as an example, wants their entire manufacturing supply chain to be 100% renewable by 2030. Through their renewable energy initiative, in August 2020, TSMC, an Apple supplier, signed the largest corporate renewable energy purchasing power agreement ever with a 920 MW offshore windfarm in Taiwan.

4. Technology sector: hardware may enjoy more tailwinds

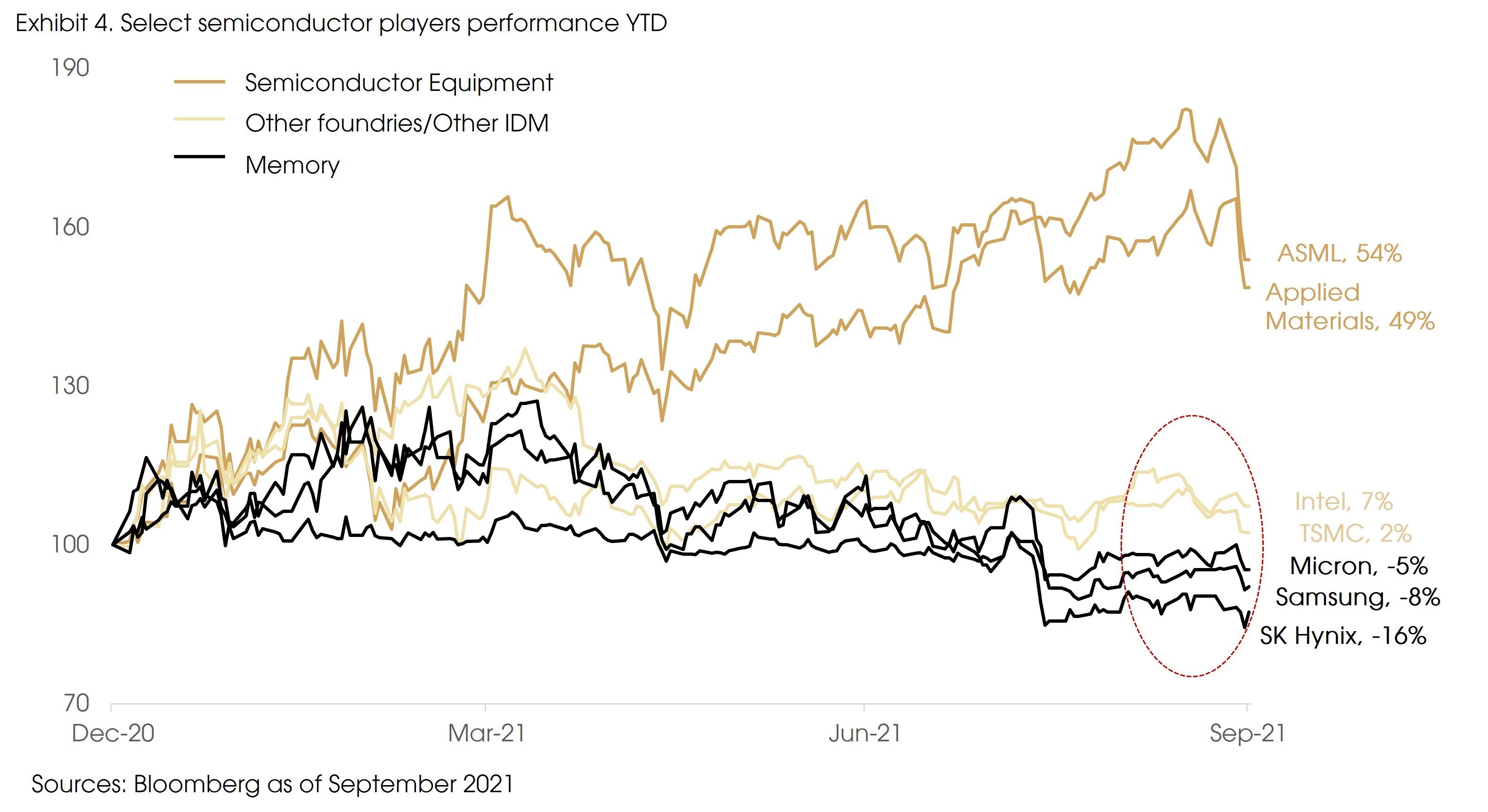

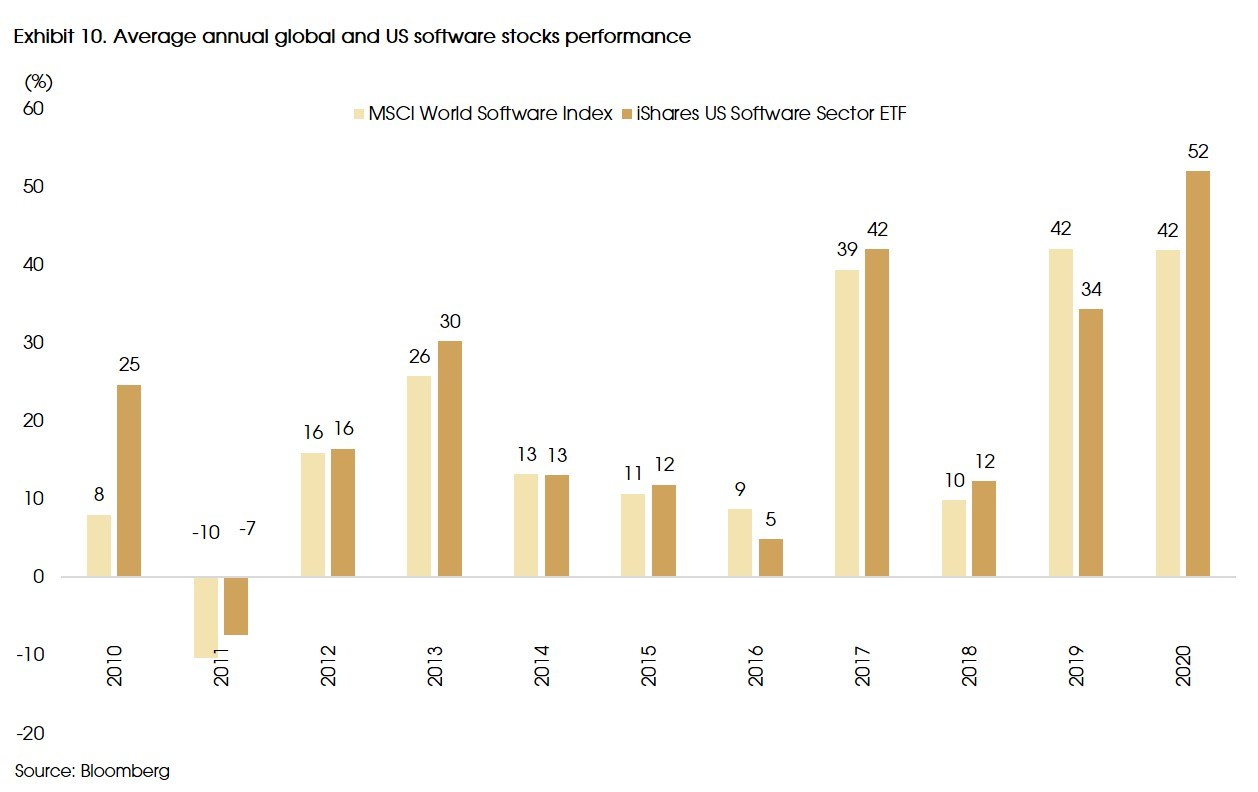

The year of 2020 saw strong outperformance of the technology sector as COVID-19 accelerated global digitalization efforts. Across the subsectors of tech, software has continued its four-year gains as it posted a massive increase. Going into 2021, against the backdrop of sky-high valuation, we are cautious with the growth to value rotation, hence, we favor cyclical semiconductors with attractive secular outlook from end markets such as 5G smartphones, IoT, Autonomous Vehicles, and Gaming.

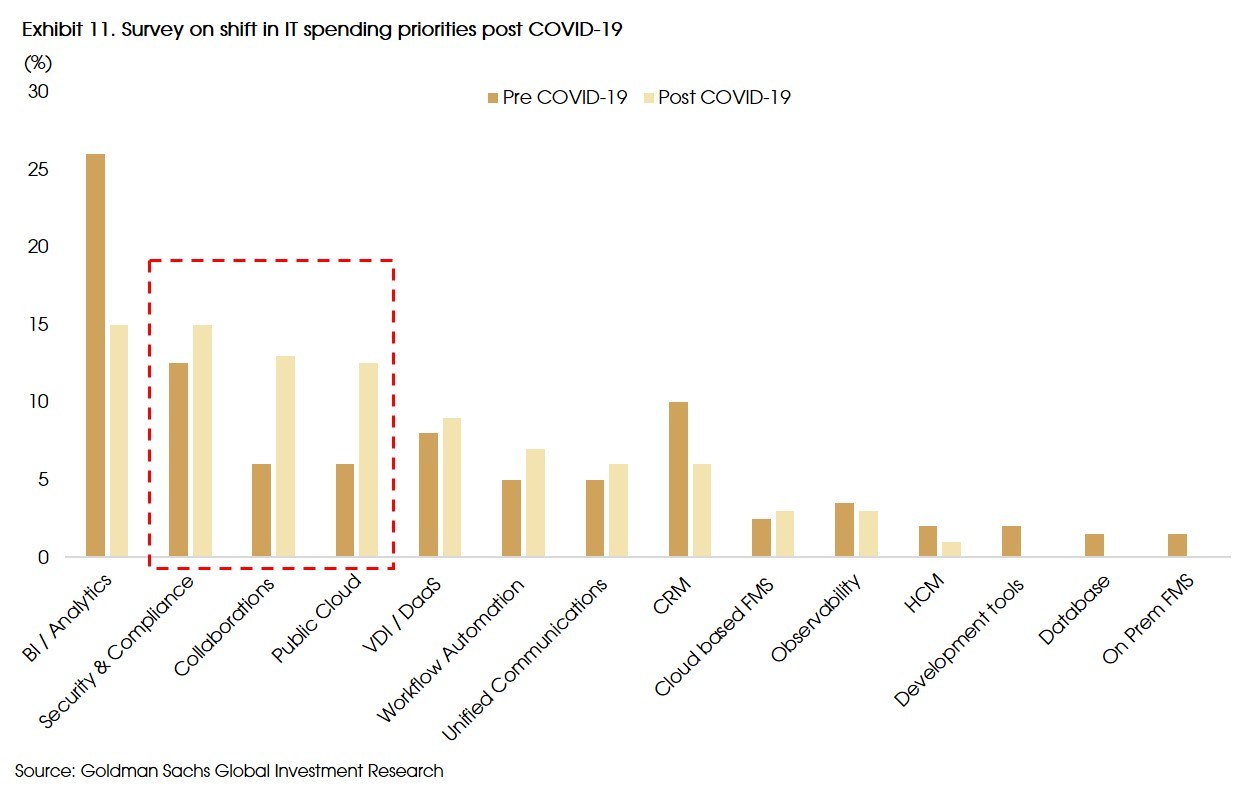

Over on the software side, notable increases in prioritization are being placed on areas such as public cloud, security & compliance as well as collaboration softwares. As such, we believe demand should continue to pick up for cloud infrastructure as penetration remains low at estimated ~20% of Total Addressable Market of USD 1,172 billion (GS Estimates).

We continue to like cybersecurity as part of our thematic approach. The trend of accelerating public cloud adoption and a more distributed workforce are driving a shift towards perimeter-less security architecture as enterprises rethink their cyber defense approach. Last year’s SolarWind incident, which was dubbed as one of the most significant cyberattacks in history, also provides further catalyst to the theme from cyber defense policy reform impact as well as escalation of enterprises’ cyber security spending awareness and priority.

We think that it’s still too early to tell on the future US-China trade relations. President Biden is clearly not rushing to reverse current sanctions imposed on Chinese tech companies. While analysts are expecting a more diplomatic approach from the Biden government, early indicators from the US top officials hinted that the US-China saga may likely to continue. The ongoing anti-trust scrutiny across US, EU, and China hinders us from developing a positive view towards Big Tech names.

5. Healthcare sector: selectively positive

We are selectively bullish on healthcare in 2021. We think that investors will prioritize individual company’s innovation when investing into pharmaceuticals and biotechs. We remain positive on the medical devices sub-sector and are tentatively optimistic on telemedicine.

The US political risks that faced healthcare stocks have moderated as Democrats and Republican have not gained any significant majority in Congress, which we feel is required to pass sweeping legislation. The temporary removal of this political overhang causes us to believe that investors may revert to concentrating on the drug pipeline for both pharmaceuticals and biotechs.

As scientific knowledge advances, new medical solutions are developed to address unmet medical needs or create improved solutions. The number of drugs approved by the US FDA between the five-year period of 2015-2019 was 220 which is a 40% increase from the previous five-year period of 2010-2014. However, these figures do not address the increasing importance and accommodative policies that the Chinese government is placing on research and development in the biotech sector locally. We expect that China’s biotech sector will continue to develop through 2021 with certain companies emerging as noteworthy global players.

The importance of medical equipment and devices was emphasized in 2020, particularly with the importance of diagnostics testing supply chain for monitoring the COVID pandemic. We believe these companies will continue to play a significant role in 2021 as testing is still vital throughout the vaccination roll-out. Moreover, post pandemic we think that governments may invest more into their public health infrastructure. This could be through stocking up on personal protective equipment, improving infectious disease detection and pandemic preparation. This should be a longer-term positive for this particular sub-sector.

The pandemic contributed to a surge in demand for telemedicine globally. Particularly, as regions were in lockdown, patients and doctors were forced to opt out of in-person visits, which also helped familiarize themselves with this concept. Although the benefits of telemedicine in improving the healthcare accessibility and reducing costs are undeniable, our caution is on the sustainability of the growth post pandemic. Specifically, we are unsure, whether individuals in larger developed cities with easy access to healthcare, will continue to be customers of these platforms.

6. Consumer sector: optimistic on discretionary spending

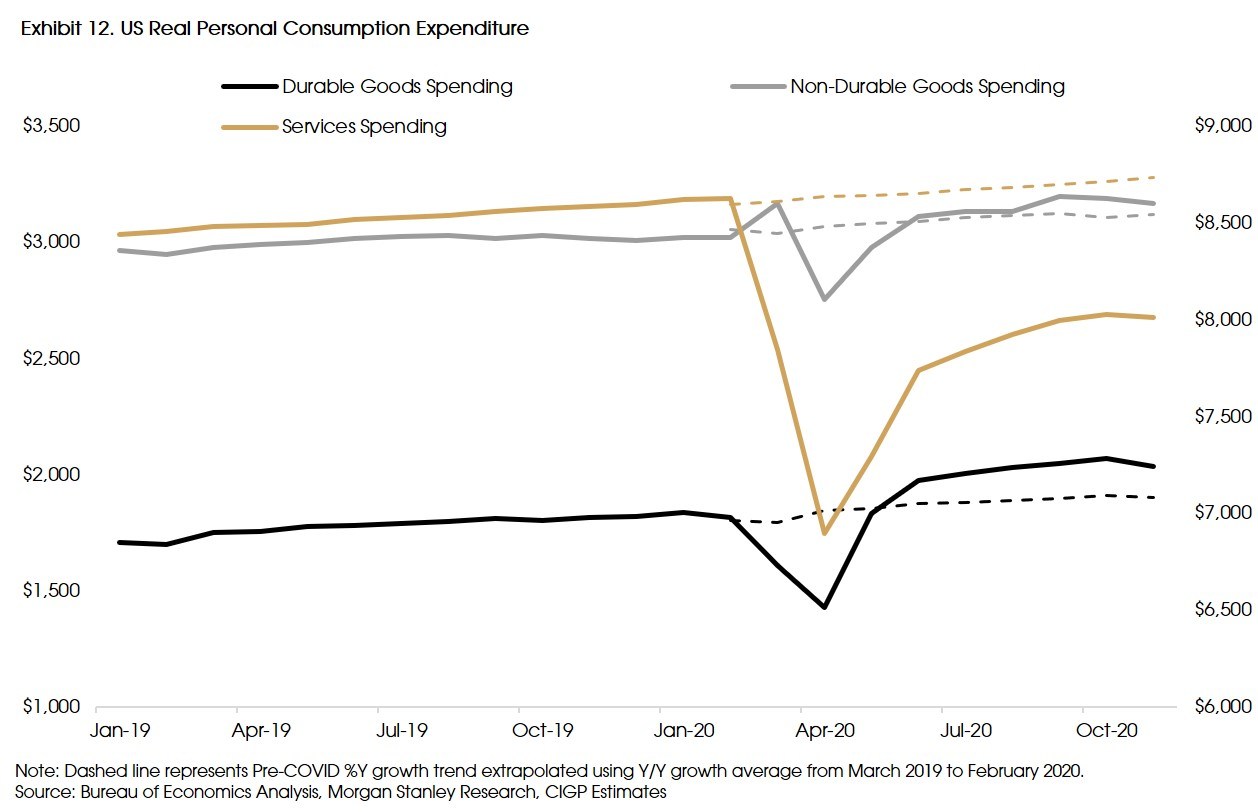

The overarching sentiment within consumer sector is largely dependent on the strength of recovery post vaccination efforts going into 2021. We are bullish on consumer discretionary such as luxury goods and segments which are prime beneficiaries from return to normalization. Encouraging improving indicators such as global retail sales and US personal consumption expenditure data helped us to developed a more optimistic view towards discretionary spending habits.

We take more caution on consumer staples in light of rising commodity prices, which will increase pressures on margins. Within staples, we note the attractiveness of beverages as normalization continues, and we think consumers returning to dine-in as an inevitable event.

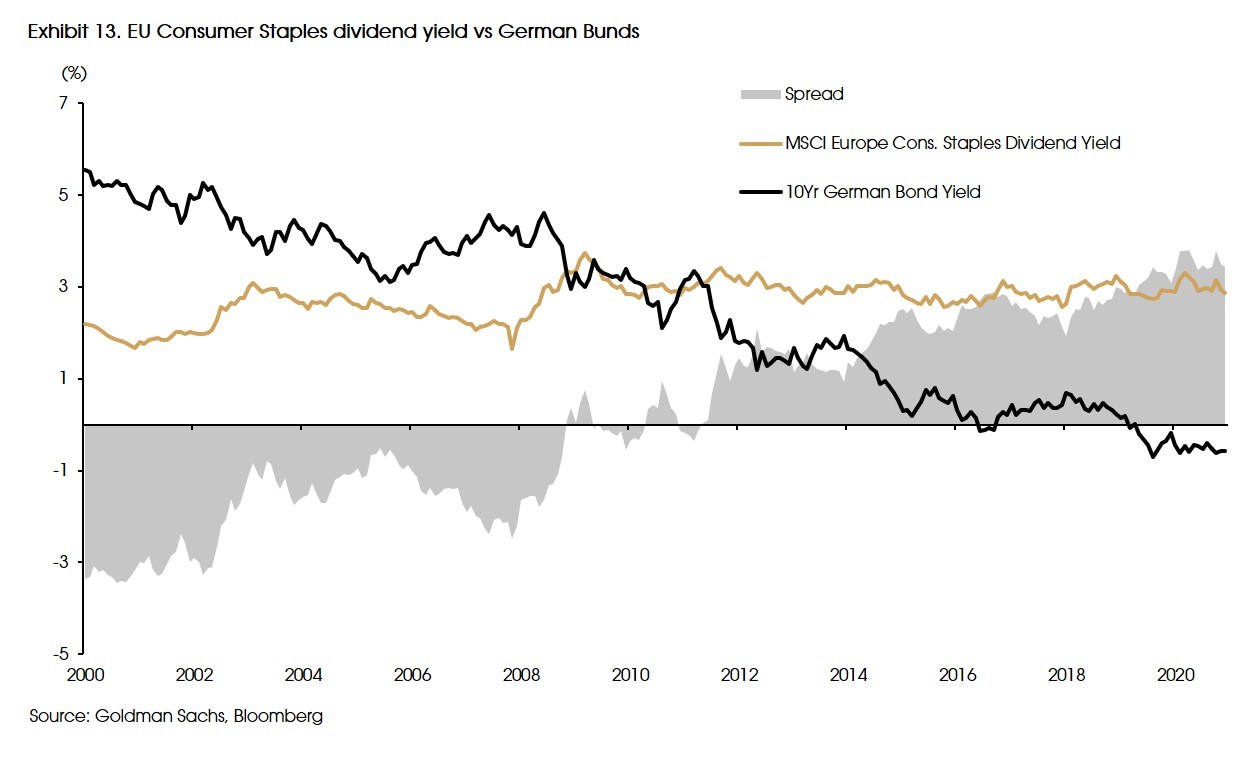

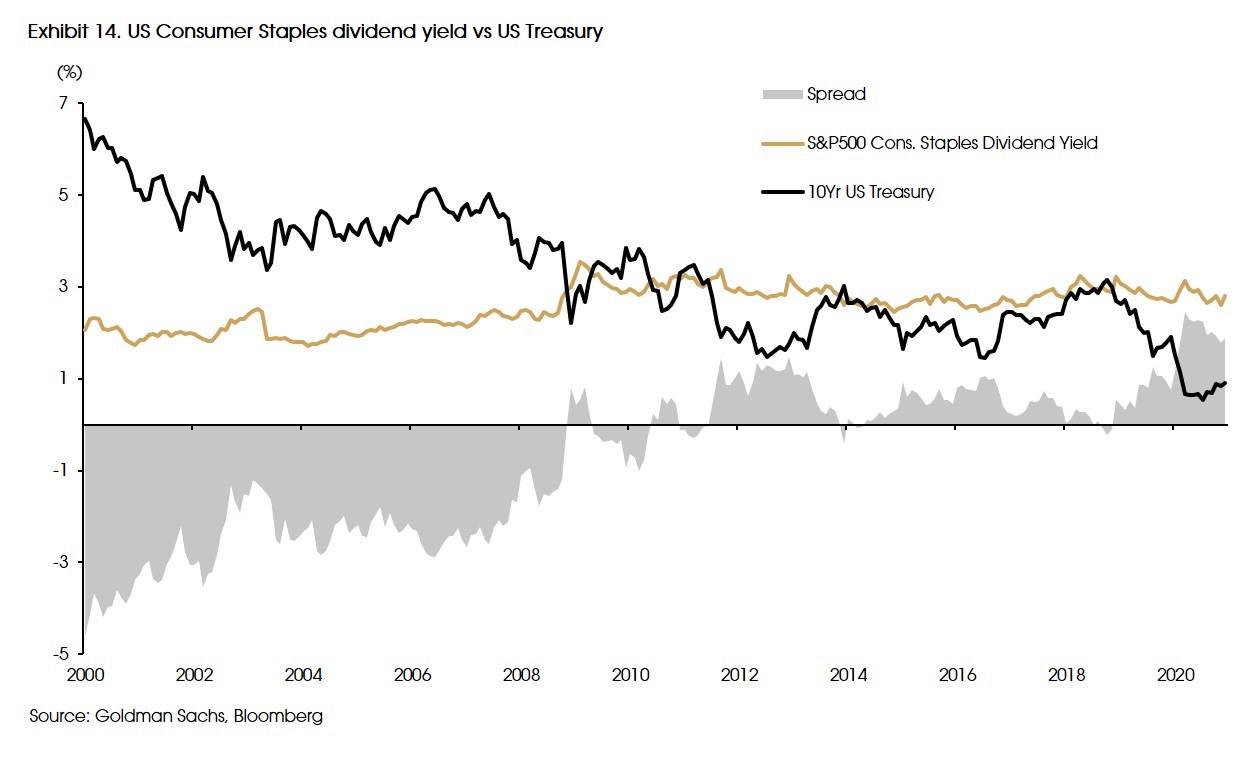

Albeit looming risks from inflation and rising rates, consumer staples companies with strong cash flow generating capabilities still provide decent dividend yields, which is well above bond yields. Thus, we still see opportunities in this sector. In general, consensus estimated a mid to high single digit top line growth with a double digit rebound for earnings in consumer staples.

We’re hopeful with the potential rebound in demand among Emerging Markets consumers, where we see more long-term opportunities for this segment. However, as the biggest EM consumer markets are countries which have been hardest hit by the pandemic, such as Brazil, India, and Indonesia, we are more optimistic towards local consumer brand names in China, as the domestic consumption play remains very strong.

The pandemic has brought about changes in consumer habits and pushed companies to rethink their business model. While most of the transformations was incepted as businesses enter survival mode, we believe certain trends are here to stay, paving the way for structural shifts in the sector. These are areas such as online food delivery, curbside pickups, e-commerce strategies, direct to consumer channels, etc.

7. 2021 Prediction List Summary